New York City’s pension funds just executed the largest private equity secondaries sale in history, a $5 billion portfolio offload led by Blackstone. For many, it’s just another headline. But for those watching the deeper currents in capital markets, it’s something more: a signal that even long-term, illiquid capital is being reshaped by today’s debt-heavy, cost-conscious world.

The Transaction at a Glance

- Deal Size: $5 billion

- Stake Type: Legacy private equity fund interests

- Buyer: Blackstone (acquiring over 95% of the portfolio)

- Managers Involved: Over 125 funds from 74 firms

- Post-Sale Count: Now streamlined to ~45 active Genral Partner (GP) relationships

NYC’s CIO, Steve Meier, noted that some holdings dated back to 2007 and 2008, products of what he calls PE’s “Golden Age.” But this sale isn’t just historical housekeeping. It’s a window into how large Limited Partners (LPs) are evolving.

What This Means: Strategic Realignment > Liquidity Grab

While some observers see secondaries as a liquidity release valve during cash-strapped cycles, this deal is more nuanced. NYC wasn’t forced to sell. It chose to. The move speaks to:

- A desire to simplify manager rosters

- Greater appetite for co-investments

- Operational cost savings

- More tailored portfolio management across its 5 pensions

Debt Pressure and Institutional Behavior

What’s happening at the macro level adds even more color to this story.

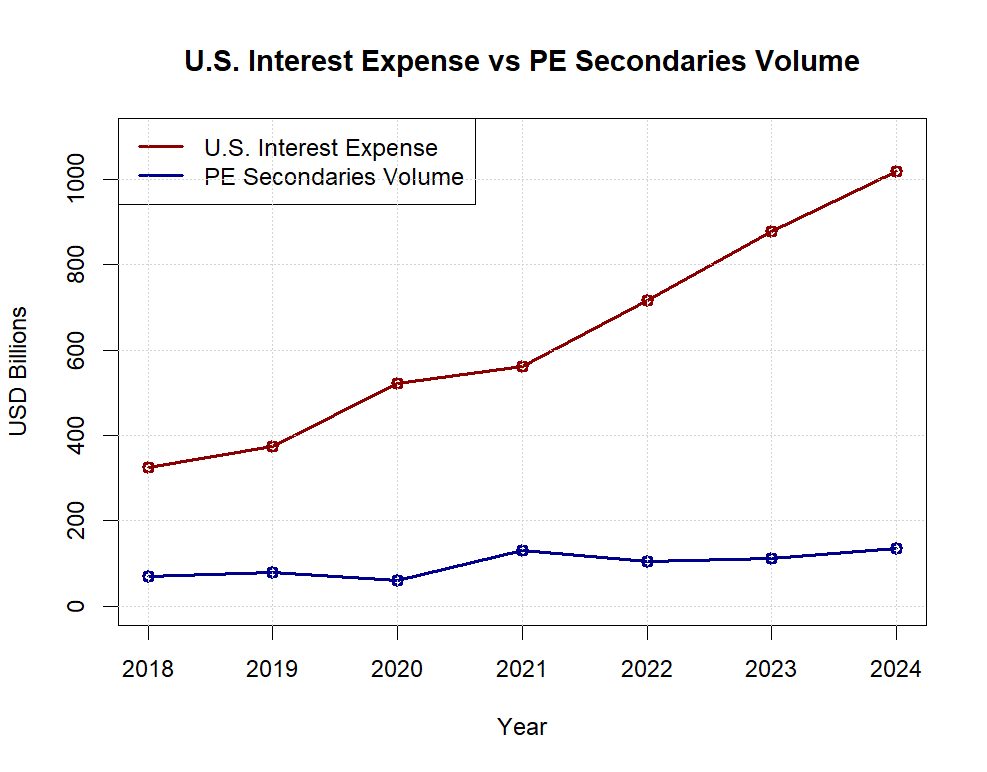

U.S. interest expenses have topped $1 trillion annually — a staggering weight that has refocused asset allocators everywhere on capital discipline, cost of carry, and liquidity flexibility.

NYC’s $5B exit is part of a broader theme: capital conservatism in an era of rising debt. With tighter funding conditions, LPs are:

- Trimming complex portfolios

- Avoiding over-diversified exposure

- Favoring fewer, deeper relationships

Macro Meets Micro

Here’s how rising debt pressure and institutional realignment may be playing out in tandem1:

Why It Matters for the Industry

- Emerging managers may struggle more to raise capital from LPs trimming their GP count.

- Secondaries markets will heat up as more pensions and sovereigns reevaluate legacy commitments.

- Co-investment will surge, but only where LPs feel confident enough to take a seat at the deal table.

NYC’s landmark deal isn’t just a one-off. It’s a playbook. As global capital costs climb, expect more pensions, endowments, and insurers to rewire their private capital strategies. Fewer names. Deeper trust. Greater flexibility.

In the age of expensive debt, even the most patient capital has a clock.

- Sources: U.S. Department of the Treasury (Monthly Statement of the Public Debt, 2018–2024), Congressional Budget Office (Budget Projections, 2023–2025), Greenhill Global Secondary Market Trends (2020–2023), PitchBook Private Markets Monitor (2023), and Preqin Global Alternatives Reports. ↩︎